As Jean Monnet said, “Europe will be forged in crises and will be the sum of the solutions adopted for these crises“, and, once again, Europe and NATO will have to face a new season of crises, that has aptly been described as a permacrisis. Let us first quickly draw a global macroeconomic picture based on the IMF’s forecasts. We know the economy can be fallible in forecasting, but when the going gets tough, it’s best to be cautious.

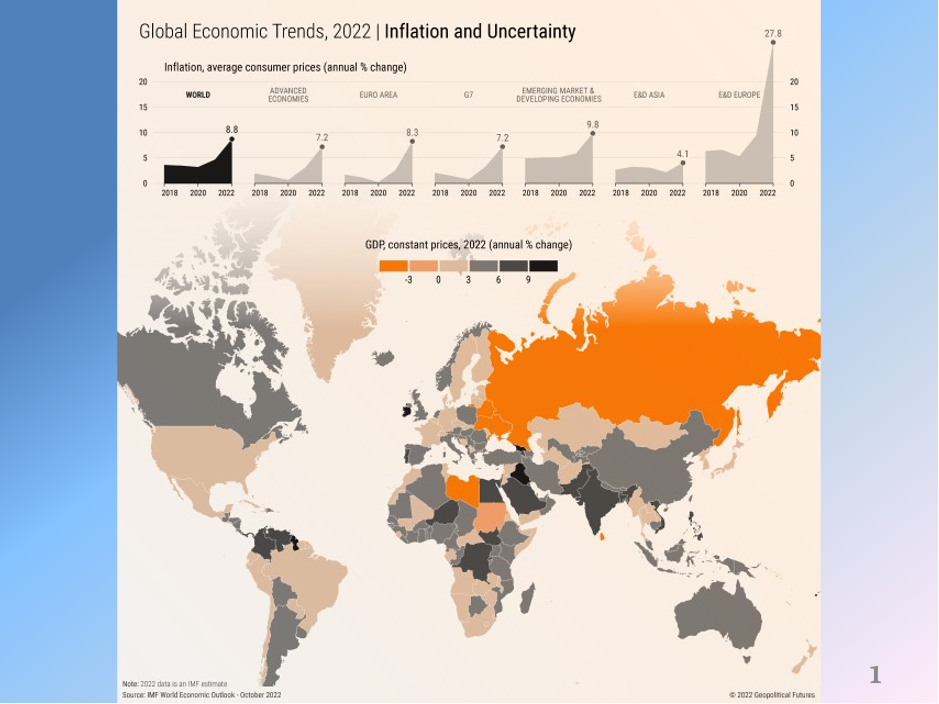

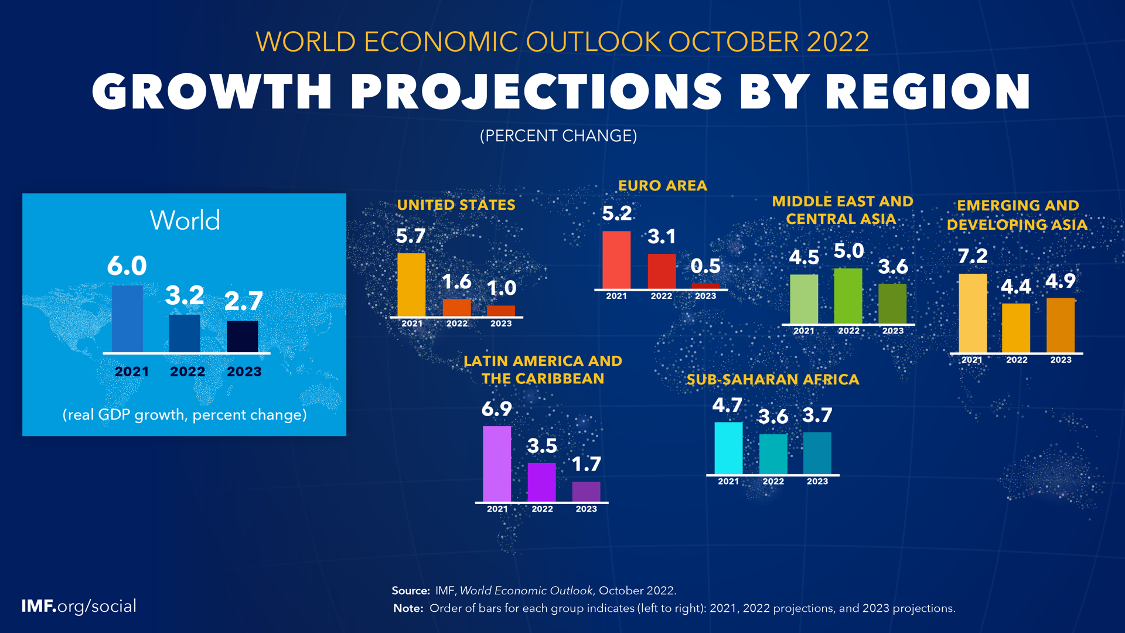

These three graphics are quite useful to summarise the situation.

In the 2022 World Economic Outlook the conclusions are quite clear:

“Policy paths in the largest economies could continue to diverge, leading to further US dollar appreciation and cross-border tensions. More energy and food price shocks might cause inflation to persist for longer. Global tightening in financing conditions could trigger widespread emerging market debt distress. Halting gas supplies by Russia could depress output in Europe. A resurgence of COVID-19 or new global health scares might further stunt growth. A worsening of China’s property sector crisis could spill over to the domestic banking sector and weigh heavily on the country’s growth, with negative cross-border effects. And geopolitical fragmentation could impede trade and capital flows, further hindering climate policy cooperation”.

All this means that, even managing to avoid another global crisis (the third after that of 2006 and the pandemic), the combination of stymied growth, monetary rigour, inflation and other geopolitical factors already mentioned, would drastically reduce financial resources not only for a possible Ukrainian reconstruction plan, but for that defence expenditure which is objectively necessary.

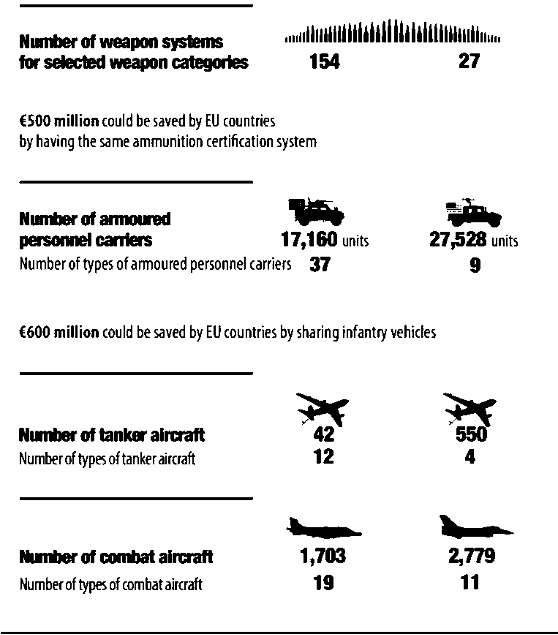

In this already difficult picture, it is important to draw the attention on some few important factors in the expected arms procurement, if we are to ensure credible deterrence:

All EU (and NATO) countries have an urgent need to replenish previous military donations and to massively increase ammunition stockpiles, because we have seen how much ammunition has been consumed in this conflict. Rough Russian estimates speak of 3,6 million 152 mm shells fired in five months, for example;

The 2% criterion regarding the Defense expenditure/GDP ratio has always been an indicative criterion: now what matters is the purchase of concrete capabilities, i.e., weapon systems useful for the defence of NATO and national territory, with an effective logistic supply of spare parts and ammunition, as well as with a concrete availability of trained personnel: we have seen that an army of 100.000 fighters lasts for about eight months of medium intensity operations;

Even by increasing defence funds, a recurring phenomenon in all European armed forces, with some rare exceptions, consists in still financing weapon systems that were suitable for managing crises, possibly overseas, avoiding the reconstitution of that heavy or high fire potential that is necessary in deterrence and/or defence;

Those European countries that have disposed of Soviet systems to supply Ukrainian forces are typically markets already captured by non-EU, and sometimes not even NATO suppliers, who have the advantage of lower unitary prices.